Welcome to Part 3 of our Tax Series focused on the taxation of Family Business Enterprises.

For many successful families, the family business is more than a commercial venture; it is a legacy that carries identity, history, and continuity across generations. But as Nigeria’s fiscal landscape evolves, even legacies must adapt. The 2025 Tax Acts have introduced significant changes that will reshape how family-owned enterprises are structured, taxed, and sustained, and understanding these changes is essential to preserving both value and reputation.

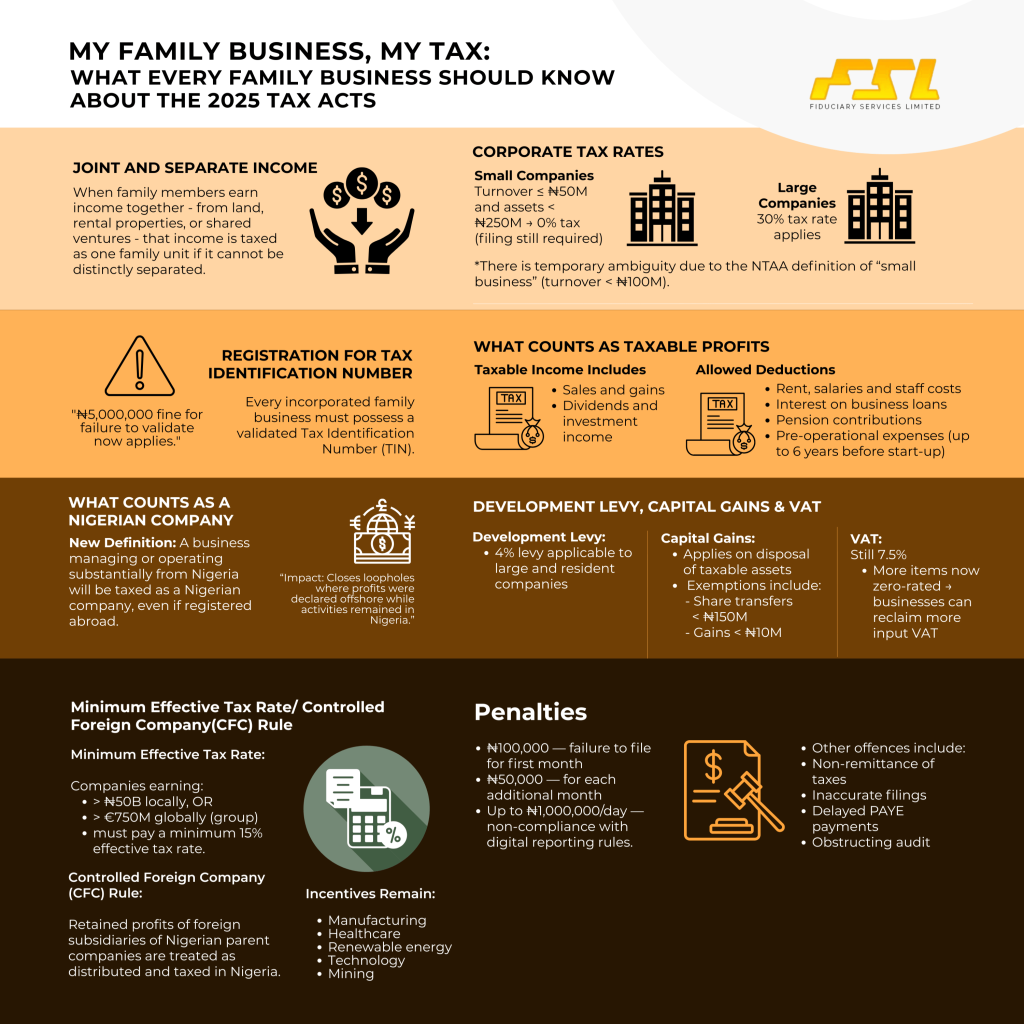

Joint and Separate Income

Family enterprises are unique because business and personal interests often intertwine. Under the new regime, where family members jointly earn income, for instance, from family land, rental properties, or a shared venture, and those earnings cannot be distinctly separated, the income will now be treated as family income and taxed as one unit.

However, income from inherited property, shares, or investments remains exempt from this family classification until it is distributed to individual members, at which point each person assumes responsibility for their portion. It is a fine but important distinction, designed to ensure fairness and transparency.

Registration for Tax Identification Number

For incorporated family businesses, compliance begins with registration. Every company must possess a Tax Identification Number (TIN), now automatically issued by the Corporate Affairs Commission upon registration. However, validation remains the company’s responsibility. Ignoring this step attracts a fine of ₦5,000,000, a reminder that tax identity is now as vital as legal incorporation. The TIN must appear on all correspondence, filings, and business documents, and financial institutions, brokers, and insurers are equally bound to reject transactions without it. It is also now an offence for a company to award a contract to a person without a Tax ID.

Definition of a Nigerian Company

Another significant shift in the Acts concerns what qualifies as a Nigerian company. Even if a business is registered abroad, if its management or core operations occur in Nigeria, it will now be taxed as a Nigerian company. This redefinition closes the long standing loopholes that once allowed profits to be booked offshore while operations remained onshore.

Tax Rates

As for corporate tax rates, the Acts take a tiered approach. Companies with annual turnover of ₦50 million or less and assets under ₦250 million qualify as small companies and enjoy a 0% tax rate, though they must still file returns. Larger entities pay 30% on profits. Some ambiguity remains, however, as the Tax Administration Act (NTAA) 2025 defines “small businesses” differently, as those with turnover below ₦100 million, though this is pending further regulatory clarification. What is certain, however, is that professional service firms, regardless of income level, no longer qualify for small company relief and must pay the full tax rate.

Taxable Profits and Deductions

Furthermore, in determining taxable profits, companies must compute income from all sources: sales, gains, dividends, and then deduct eligible business expenses. The Acts allow deductions for rent, staff costs, interest on business loans, pensions, and legitimate pre-operational expenses incurred within six years before start-up. Even corporate generosity is recognized: donations to approved charitable, educational, or public institutions qualify for deductions of up to 10% of profit before tax, while non-cash donations may also qualify for a deduction at the lower of the cost price of the item at the time of purchase or prevailing market value. Research and Development (R&D) expenditure remains deductible up to 5% of turnover, rewarding innovation within the private sector. Personal or unrelated expenses, however, remain strictly excluded. Only expenses that directly enable income generation count toward reliefs. The law’s intent is clear: profits must reflect true business performance, not personal spending disguised as operations.

Development Levy, Capital Gains and Value Added Tax (VAT)

Beyond corporate tax, development and capital gains obligations also apply. Large and Resident companies must now pay a 4% Development Levy, and all companies pay chargeable gains on disposals of assets that attract tax, except for the sale of shares below ₦150 million or where the gain is under ₦10 million. The Value Added Tax (VAT) rate remains 7.5%, but the list of zero-rated items has been expanded, allowing qualifying businesses to recover more input VAT.

Minimum Effective Tax Rate/ Controlled Foreign Company(CFC) Rule

For groups with multinational operations, the landscape has become even more sophisticated. The Acts introduce a 15% minimum effective tax rate for companies earning over ₦50 billion locally or €750 million globally. In effect, if your foreign subsidiaries pay less tax abroad, your Nigerian group must make up the difference, aligning with global tax reforms designed to prevent profit shifting to low-tax jurisdictions.

In addition, the Controlled Foreign Company (CFC) rule now deems retained profits of foreign subsidiaries of Nigerian parent companies as distributed and therefore taxable, even when those profits have not been formally paid out. On the brighter side, companies in priority sectors such as manufacturing, renewable energy, healthcare, technology, and mining continue to benefit from tax holidays and other investment incentives, particularly where reinvestment supports local growth.

Penalties

The penalties for default of these rules are steep: ₦100,000 for the first month of failure to file, ₦50,000 for each subsequent month, and up to ₦1,000,000 daily for refusal to comply with digital reporting requirements. Non-remittance of taxes, inaccurate filings, or failure to cooperate with audits can also lead to other heavy fines or imprisonment.

Tax compliance for companies today goes beyond filing. Every company must now:

- Appoint a designated tax agent;

- File annual self-assessment returns within six months of its year-end or 18 months post-incorporation;

- Submit monthly VAT returns by the 21st of the next month;

- Adopt the new electronic fiscalisation system, ensuring transparent invoicing and data reporting;

- Report any changes in shareholding, ownership, or registered address;

- Disclose any tax planning arrangements to the authorities; and

- Remit PAYE and employee deductions promptly.

The message is unmistakable: tax compliance has become integral to governance. For family-owned enterprises, these laws are not merely administrative; they are structural. This requires not only understanding the statutory obligations but also leveraging available incentives, reliefs, and exemptions in a way that aligns with the family’s long-term vision. They require a thoughtful review of business processes, documentation, and intergenerational governance. As the fiscal environment grows more transparent, families that act early, updating records, reviewing entity structures, and engaging professional estate planners, tax, and legal counsels will be best positioned to preserve wealth while staying ahead of regulatory expectations.

In the next part of this series, we will explore how the 2025 Tax Acts shape the realities of the global Nigerian, examining the tax obligations of individuals and families with global assets, dual residencies, international business interests, and non-resident entities connected to Nigeria.

As part of our Wealth Preservation services, we have experienced Advisors ready to assist you in developing an estate plan that protects, preserves, and sustains you and your family’s wealth for generations.

Get in touch with one of our professionals today by sending an email to contact@fiduciaryservicesltd.com.